Supply chain system shock

The world has never been so volatile..or has it?

Last week, the Easter holiday closed out the first quarter of 2026, bringing to an end three turbulent months of geopolitical conflict that have affected millions of civilians and disrupted global supply chains.

The impact has been vast. Starting with tit for tat tariffs between the US and China, the expansion of “friendshoring” and culminating in the devastating war between the US, Israel and Iran and the separate but equally devastating Israeli attacks on Lebanon.

I’ve written previous articles on the crushing impact this is having on supply chains and the knock-on effects for the aid and food systems, but this week I was considering how significant these shocks were from a global historical basis, and can you even measure that?

Which events over the last 50 years delivered the biggest supply chain shocks

So, don’t hate me, but I used AI to prepare this list below. I never use AI to write this newsletter, but it would take hours to compile something like this myself, and I simply don’t have enough hours in the day. I haven't validated it, so at best we can consider it illustrative.

Generated by AI with the prompt - “give me one shock per year for the last 50 years that impacted global supply chains, be brief”

1976–1985

1976 – Aftershocks of the 1973 oil crisis continue to reshape global energy supply chains

1977 – Containerisation expands rapidly across global ports

1978 – Chinese economic reforms under Deng Xiaoping begin

1979 – Iranian Revolution disrupts global oil supply

1980 – Iran–Iraq War begins, impacting oil shipping

1981 – IBM launches the personal computer, accelerating electronics supply chains

1982 – Latin American debt crisis disrupts global trade flows

1983 – Introduction of GPS (military) begins future logistics transformation

1984 – Global semiconductor industry expansion accelerates

1985 – Plaza Accord reshapes manufacturing competitiveness

1986–1995

1986 – Chernobyl disaster disrupts European supply chains

1987 – Black Monday financial crash impacts global trade volumes

1988 – Exxon Valdez oil spill disrupts energy logistics in Alaska

1989 – Fall of the Berlin Wall opens Eastern European supply chains

1990 – Gulf War disrupts oil flows

1991 – Dissolution of the Soviet Union reshapes global trade routes

1992 – EU Single Market launched, reducing internal trade barriers

1993 – NAFTA signed, integrating North American supply chains

1994 – WTO established, formalising global trade rules

1995 – Commercial internet expands, enabling digital supply chains

1996–2005

1996 – Growth of global contract manufacturing (Asia-led) accelerates

1997 – Asian Financial Crisis disrupts manufacturing hubs

1998 – Russia financial crisis impacts the commodities supply

1999 – Y2K drives global IT and supply chain system upgrades

2000 – Dot-com crash impacts tech supply chains

2001 – September 11 attacks disrupt global aviation and trade

2002 – US port lockout disrupts West Coast supply chains

2003 – SARS outbreak disrupts Asian supply chains

2004 – Indian Ocean tsunami disrupts regional logistics

2005 – Hurricane Katrina disrupts US energy and logistics

2006–2015

2006 – Expansion of mega container ships reshapes shipping economics

2007 – Global food price crisis disrupts agricultural supply chains

2008 – Global Financial Crisis collapses trade volumes

2009 – H1N1 pandemic impacts global travel and logistics

2010 – Eyjafjallajökull eruption halts European air freight

2011 – Fukushima nuclear disaster disrupts electronics and automotive supply chains

2012 – US drought impacts global food supply chains

2013 – Rana Plaza factory collapse reshapes apparel sourcing

2014 – Russia annexes Crimea, triggering sanctions and trade shifts

2015 – Volkswagen emissions scandal disrupts automotive supply chains

2016–2025

2016 – Brexit referendum creates long-term trade uncertainty

2017 – US withdraws from TPP, reshaping Asia-Pacific trade alignment

2018 – US–China trade war begins with tariffs imposed

2019 – US–China tariffs escalate across multiple sectors

2020 – COVID-19 pandemic shuts down global supply chains

2021 – Suez Canal blockage by Ever Given halts global shipping route

2022 – Russian invasion of Ukraine disrupts energy, grain, fertiliser

2023 – Red Sea shipping disruptions begin due to attacks on vessels

2024 – Panama Canal drought restricts vessel transits

2025 – Escalation of the Middle East conflict disrupts Hormuz and regional logistics

So, how would you objectively compare these shocks to see which has the biggest impact, and which indicators would you use?

Measuring the “supply chain shock” factor

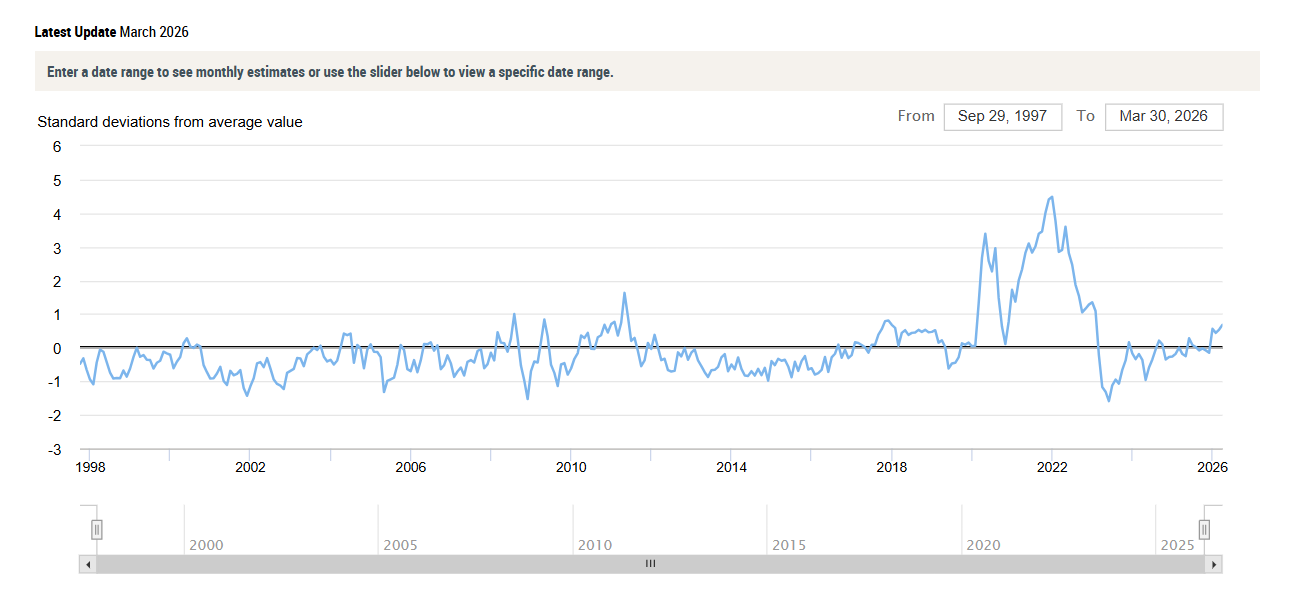

The first indicator I found to measure supply chain shock was the Global Supply Chain Pressure Index.

See below for the rationale behind this indicator and what it measures.

The goal behind constructing the Global Supply Chain Pressure Index (GSCPI) was to develop a parsimonious measure of global supply chain pressures that could be used to gauge the importance of supply constraints with respect to economic outcomes. Related research indicates, for example, that changes in the GSCPI are associated with goods and producer price inflation in the United States and the euro area, both during the pandemic period and stretching back to 1997 (the starting point of the dataset).

The GSCPI integrates a number of commonly used metrics with the aim of providing a comprehensive summary of potential supply chain disruptions. Global transportation costs are measured by employing data from the Baltic Dry Index (BDI) and the Harpex index, as well as airfreight cost indices from the U.S. Bureau of Labor Statistics. The GSCPI also uses several supply chain-related components from Purchasing Managers’ Index (PMI) surveys, focusing on manufacturing firms across seven interconnected economies: China, the euro area, Japan, South Korea, Taiwan, the United Kingdom, and the United States. For complete details on the data and methodology used to construct the GSCPI, see the foundational Staff Report.

Below you can see the indicator over the last twenty years or so, with the major spikes being the global financial crisis (2008), the Japan earthquake (2011) and the Covid pandemic (2020-2021).

The indicator has not yet been updated to reflect the impact of the latest war in the Middle East and how it compares to recent major shocks like Covid.

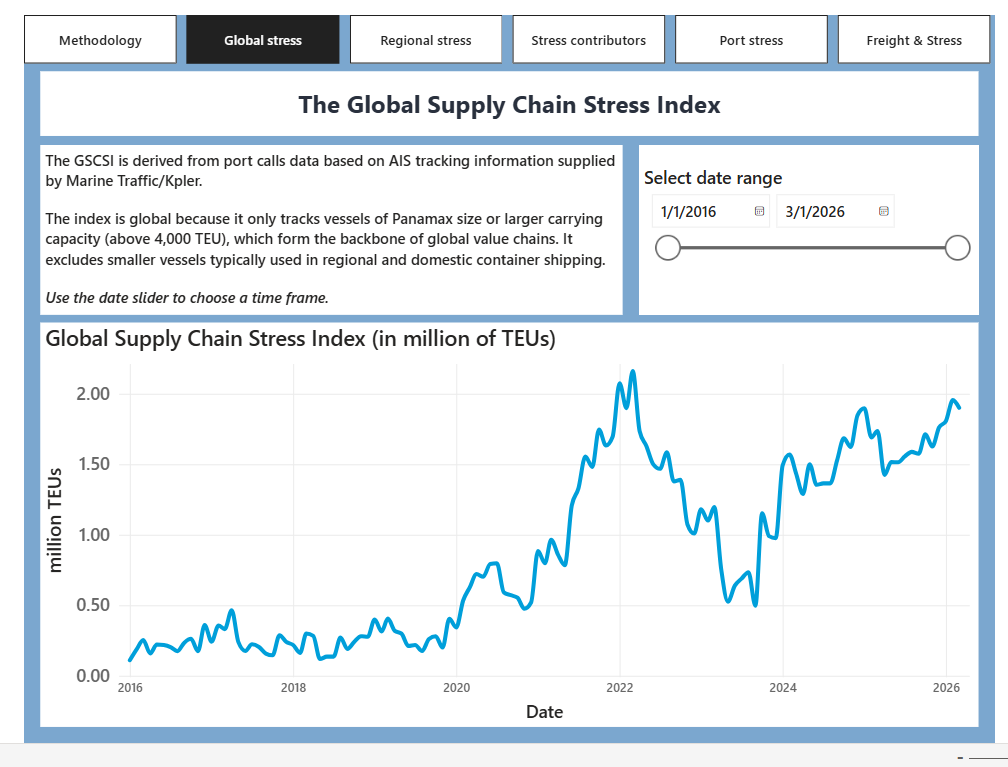

The second indicator was the Global Supply Chain Stress Index that comes from the World Bank. This one appears to be about container port challenges: measuring delays at the port level and aggregating them into an overall indicator expressed in millions of TEUs under stress.

This data shows increasing turbulence since the start of COVID (2020), and with additional peaks most likely caused by tariff wars, showing through 2024-2026. This indicator was last updated in early March, so I would expect the trend to continue up when measured in April.

These two indices interpret underlying data to produce a global index that aims to compare relative shocks.

But actually, they probably aren’t that useful day to day for assessing supply chain stress and its impacts on a specific supply chain. No one runs a truly global supply chain; we are all exposed to different regions, lanes, modes, and at different times and in different years, so looking at more detailed, localised data is the way to understand how important shocks are.

Finding indices that track prices on lanes you are particularly exposed to, perhaps helps you to understand supply and demand on your particular lane, or tracking port congestion for your critical hubs or demand on your particular container routes. If you rely on commodities, then tracking the spot prices of those commodities may be your best route.

A shock to a single lane on which you are reliant and have no contingency can destroy your supply chain, but would not register on the charts above as globally significant.

So are we in the most turbulent of times globally?

According to the indicies then no, not even the most impactful in the 2020’s. I’m also sure that if you spoke to someone in 1919 or 1942, then the level of global turbulence today would seem relatively small compared to what the world was dealing with back then. The extent to which the current Middle East war disrupts global supply chains will depend on whether the ceasefire holds and, therefore, on developments in the Straits of Hormuz and the Bab El Mandeb. A prolonged war for months may lead to spikes that dwarf those seen in recent times.

I can’t end without repeating what I always say: you can’t measure impact purely in metrics, lead times, and supply chain disruptions. Millions of children globally are living under horrific conditions caused by conflicts that could be resolved. Whether in internal factional conflicts or regional or global conflicts, if we put people first and set our own desire for power aside, then it would be possible to build a better world.

I hope for an end to conflicts that impact millions of children around the world and a return to normality, where supply chain shocks affect only companies' bottom lines, not household budgets or children’s lives.